Siemens Energy: Positioned for the Electricity Supercycle

Bottom Line

Siemens Energy is not in a normal cycle: the global electricity buildout is a multi-decade trend

Gas and grid infrastructure are essential for data centers and renewable energy stability

Strong growth outlook: EPS is expected to increase roughly 4× by 2028, while margins continue to expand

Risk remains at Siemens Gamesa, but the company’s core cash-generating businesses are strong

Valuation remains cheaper than peers, creating an attractive risk-reward setup

The opportunity

Siemens Energy is an industrial company that sells gas turbines and electricity grid infrastructure. At first glance, it appears to be a traditional cyclical industrial business. I believe that view is outdated.

We are not in a normal cycle. We are in a multi-decade electricity infrastructure buildout.

Gas is playing a vital role in meeting rising electricity demand, particularly for data centers. While the market focuses heavily on nuclear energy as the long-term solution, the short- to medium-term supply of reliable power is largely coming from natural gas. Gas turbines can ramp quickly and provide the stability needed in renewable-heavy power systems.

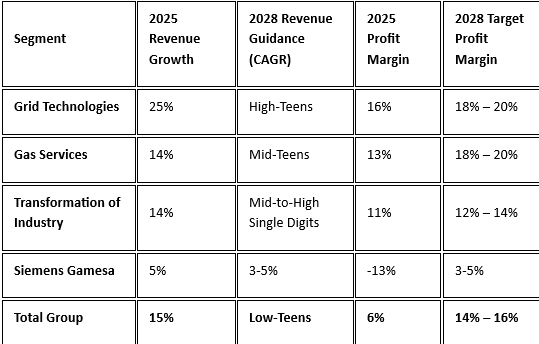

The company is guiding for mid- to high-teens revenue growth and meaningful margin expansion through 2028. Earnings per share are expected to increase roughly fourfold by fiscal 2028, creating significant operating leverage.

The wind division, Siemens Gamesa, remains a risk, and the turnaround is not yet fully complete. However, even with that overhang, Siemens Energy is trading at a discount to its direct peers, GE Vernova and Mitsubishi Heavy Industries.

The valuation is not demanding, and if earnings develop as guided, profit growth alone can deliver an above-benchmark return.

Business model overview

Below I’ve summarized the main business segments in which Siemens Energy operates.

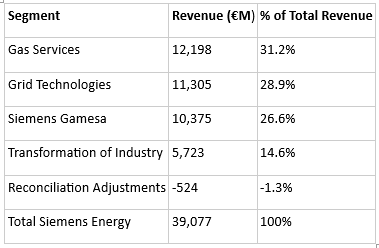

Siemens energy business segments per end of fiscal 2025

Gas Services: The Cash Engine

Gas Services primarily sells gas turbines and steam turbines. A gas turbine is a type of engine that generates electricity by burning fuel—usually natural gas—and using the hot gases produced to spin a turbine, which then drives a generator. These turbines are widely used in power plants because of their efficiency and ability to respond quickly to changes in electricity demand.

The company also offers aeroderivative gas turbines, which are essentially gas turbines resembling jet engines. These units are often installed next to data centers to provide immediate on-site power. They function similarly to diesel generators but offer greater efficiency.

A steam turbine converts steam into mechanical energy, which then drives a generator to produce electricity. Steam turbines are commonly used in nuclear power plants.

Three companies effectively control the global heavy-duty gas turbine market:

Mitsubishi Heavy Industries

GE Vernova

Siemens Energy

Barriers to entry are extremely high due to the technological complexity of these machines and the decades of R&D embedded within them.

A new entrant would need to invest billions of dollars to develop a top-quality turbine. Customers also need confidence that a manufacturer can provide reliable long-term service and maintenance for one of the most complex machines in the industrial world.

Gas Services is particularly attractive because, in fiscal 2025, 64% of revenue came from maintenance and service contracts. The business model resembles that of aerospace engines: hardware is often sold at lower margins, while long-term service contracts generate the majority of profits.

In fiscal year 2025, Gas Services generated roughly 70% of Siemens Energy’s total pre-tax free cash flow, while accounting for only 31% of total revenue.

Gas Services is the company’s cash flow machine.

Grid Technologies: The Second Growth Engine

While gas turbines generate electricity, the Grid Technologies division ensures that electricity is transported safely and efficiently across the grid.

This division sells products and solutions that move electricity from generation sites to end users. Core products include:

Transformers

Circuit breakers

Switchgear

Grid stabilization equipment

Grid Technologies (GT) is Siemens Energy’s second-largest division, representing approximately 29% of group revenue.

Service accounts for just 6% of revenue, making this business more dependent on new equipment sales. As a result, operations are somewhat more cyclical. If new orders slow down, the company cannot rely heavily on recurring service revenue as a buffer.

Demand remains extremely strong. At the end of fiscal year 2025, the division reported a backlog of €42 billion, approximately four times annual revenue. This reflects structural demand rather than a temporary uptick.

As shown in the graph below, GT delivered the highest revenue growth rate of all business units in fiscal 2025, growing 25%.

Siemens energy 2025 revenue and profit metrics

What Drives Growth?

For Gas Services, the following three developments drive growth for its products.

Highly dispatchable power

Gas turbines have become highly sought after because gas-fired power generation is easy to control. Since a gas turbine can start up within roughly 10–20 minutes, it serves as an excellent backup when solar or wind generation falls short due to a lack of sunlight or wind.

Contrast that with roughly a 6-hour startup time for a coal plant and potentially multiple days for a nuclear facility.

Coal-to-gas conversion

Coal-to-gas conversion is another major growth driver. Combined-cycle gas plants are among the most efficient large-scale sources of electricity generation, while also emitting less CO2 than coal-fired facilities.

As a result, many coal-fired plants are transitioning toward gas-fired generation, increasing demand for new turbines.

Data centers

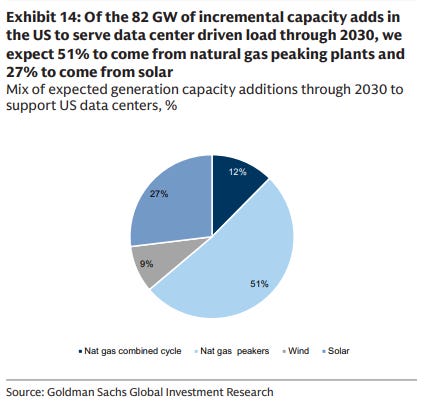

Data centers represent a major source of incremental electricity demand. According to Goldman Sachs, 63% of the additional electricity required for new data centers through 2030 is expected to come from gas-fired power generation.

Goldman Sachs expects 51% of datacenter expansions to be powered by natural gas

Growth within the GT business can largely be divided into four categories.

Growth in electricity demand

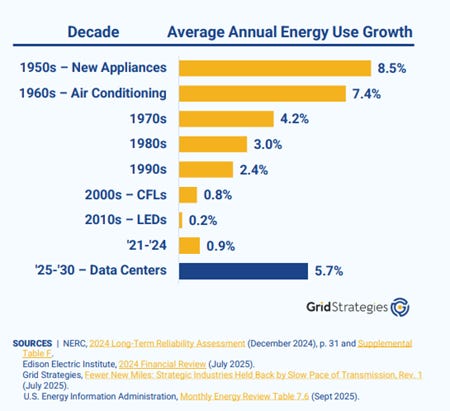

Electricity demand is rising rapidly, requiring grids to expand and modernize in order to manage higher loads. If current forecasts prove accurate, electricity consumption could grow by roughly 5.7% annually over the next five years.

That would represent one of the highest electricity demand growth periods in modern history.

Forecast of annual U.S. electricity demand growth

Aging grid infrastructure

Approximately 80 million kilometers of grid infrastructure will need renewal or expansion by 2040, roughly equal to the size of today’s entire installed grid base.

Two-way power flows

Power grids are no longer one-directional systems. Modern grids must handle decentralized generation from solar, wind, batteries, and distributed energy systems.

This requires new transformers, switchgear, and grid stabilization equipment—all products that GT supplies.

Interconnectors

Because renewable energy storage remains relatively inefficient at scale, excess electricity generated by solar or wind in one region often needs to be transported to another.

This is especially relevant in Europe, where countries increasingly rely on cross-border electricity flows. As a result, large HVDC (High Voltage Direct Current) transmission lines are being constructed, driving additional demand for switchgear, circuit breakers, and other grid infrastructure equipment sold by GT.

Both Gas Services and Grid Technologies are benefiting from long-term structural trends that appear significantly stronger than previous industrial cycles. This could allow both divisions to sustain elevated growth rates for many years.

Valuation vs. Peers

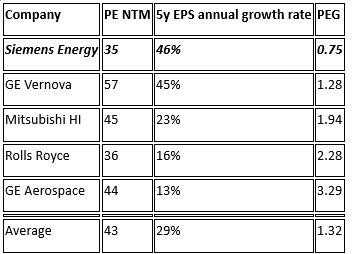

At first glance, Siemens Energy appears expensive. The next-twelve-months (NTM) P/E ratio currently stands at 37x. However, its direct competitors in the gas turbine market—GE Vernova and Mitsubishi Heavy Industries—trade at roughly 57x and 45x earnings, respectively.

I prefer looking at the PEG ratio (PE divided by growth) as well , since companies with strong earnings growth can justify higher valuation multiples.

Below, I calculated the NTM P/E ratio divided by the consensus five-year EPS growth rate. I believe this provides a better view of long-term earnings power without relying on forecasts that extend too far into the future.

On a forward PEG basis, Siemens Energy seems undervalued relative to peers. Source: Koyfin

The consensus currently expects EPS to reach roughly €7 by 2028.

If Siemens Energy maintains a next-twelve-months P/E ratio of 37x—still below most major peers—the implied share price by the end of 2027 would be approximately €288, representing a 47% compound annual growth rate (CAGR).

If Siemens Energy were to trade at the average peer NTM P/E multiple of 43x, the stock could potentially reach €301 by the end of 2027, implying roughly a 50% CAGR.

This could represent an attractive opportunity to generate alpha within a portfolio.

Risks

Siemens Gamesa

The primary operational risk remains Siemens Gamesa. In fiscal 2025, Gamesa generated negative free cash flow of approximately €3 billion.

Management’s recovery plan targets break-even by 2026 and operating margins of 3–5% by 2028.

If the turnaround fails—and Gamesa were still generating negative 5% margins by the end of 2027—EPS could decline by roughly €1 per share. Under that scenario, the implied share price would fall to approximately €222 instead of €288.

Even in that downside case, Gas Services and Grid Technologies could still deliver meaningful returns.

Execution risk is another key concern. As companies such as Rolls-Royce and General Electric have experienced, design flaws, engineering setbacks, or large investments made too late in a product cycle can lead to cost overruns, project delays, and lower profitability.

Lower data center investment

If data center infrastructure investments were to slow materially, demand for gas turbines and grid technologies could weaken.

However, electricity demand growth is much broader than AI alone. Electric vehicles, heat pumps, and the broader electrification of society provide a strong structural underpinning for long-term electricity demand.

Fixed-price contract risk

Siemens Energy also faces risk from older fixed-price contracts within its €146 billion backlog.

While newer contracts increasingly include indexation clauses that pass through inflation, remaining non-indexed projects—particularly within Grid Technologies and Offshore Wind—could pressure margins if commodity and energy prices rise sharply.

Conclusion

Siemens Energy is very well positioned for the explosive growth in global electricity consumption.

This is not a normal industrial cycle. It may become one of the strongest electricity infrastructure buildout periods since the 1950s and 1960s, when electrical appliances became widely adopted.

Historically, Siemens Energy would have been viewed as a cyclical company that experiences several years of growth followed by deceleration. Given the underlying structural drivers, I believe this opportunity is substantially larger.

Despite the inherent risks associated with industrial businesses, I believe the company’s long-term growth potential creates an attractive risk-reward opportunity.

The recent share price weakness related to the Iran conflict could provide an appealing entry point for long-term investors.