5 Insights That Shape My View on USDC stablecoin

Most investors still view stablecoins as just another crypto bet. But that framing misses what is happening. Stablecoins are on track to become one of the largest holders of U.S. Treasuries by 2030, while increasingly integrating themselves into institutional financial infrastructure.

They are addressing a global money supply of roughly $60 trillion. That’s not a niche market—it’s a massive runway for growth. In this piece, I break down five key insights that shape my view on USDC and the broader stablecoin market.

Quick take

Stablecoins are evolving from a crypto tool into a global settlement layer.

USDC is building an institutional moat.

With a ~$60T addressable market, this is a long-term compounding opportunity, not a short-term trade.

1. Stablecoins matter

First off, what is a stablecoin?

A stablecoin is a dollar converted into a digital token. The token can be exchanged for a real dollar at any time. The deposited dollars are typically invested in U.S. Treasuries by the stablecoin issuer, which earns revenue from those reserves. This is the primary revenue stream of Circle Internet Group, the company behind USDC.

The token itself is issued on a blockchain. USDC operates across several blockchains, with Ethereum and Solana being the largest. What’s important to understand is that Circle does not control these blockchains. The blockchain is a decentralized record-keeping system.

Why do we need them?

The key reason stablecoins provide value comes down to how money moves today.

Moving money still relies on multiple intermediaries, typically banks and custodians. In international wire transfers, one bank sends a message to another indicating that funds are on their way. One account is credited, another debited.

Often, several banks are involved because the sending bank may not have a direct relationship with the receiving bank.

You are effectively dealing with separate databases that do not communicate directly with one another. The longer the distance, the more intermediaries and reconciliation steps are required.

These layers create delays, which can be costly. In global trade, for instance, if funds were received instantly, goods could be released sooner.

Such delays also help explain why companies often rely on short-term financing; their funds are temporarily locked within the banking system.

Stablecoins reduce these frictions by operating on a single system: the blockchain. This acts as a global settlement layer, where both sides of a transaction exist on the same database rather than separate ones.

In financial markets, operating on a shared system also creates advantages. When you buy a bond or stock, the “asset database” and the “cash database” are typically owned by different companies. This creates uncertainty, as it takes time to verify whether the other party can fulfill its obligations.

Clearing houses exist largely to solve this problem. If one party cannot meet its obligations, the clearing house guarantees either payment or delivery of the asset.

With stablecoins, however, settlement can happen instantly while both parties operate on a shared database. This reduces reliance on clearing houses and could potentially save billions in clearing costs over time.

This is why institutions like BlackRock argue that financial markets should gradually move toward shared blockchain infrastructure.

Stablecoins are important because they operate on a global settlement layer and reduce reliance on intermediaries in payments and financial markets.

The key takeaway is that stablecoins don’t just improve payments—they reduce the need for fragmented financial infrastructure altogether.

2. Stablecoins are network-effect businesses

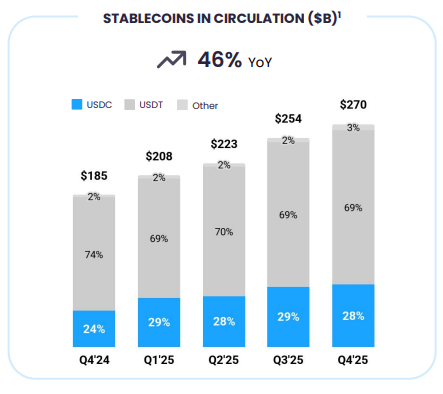

Why does Tether, an unregulated stablecoin company based in El Salvador, hold a 69% share of the stablecoin market? Its advantage comes from significant global liquidity.

Almost every cryptocurrency on major exchanges is traded against USDT, Tether’s stablecoin. To add another stablecoin trading pair such as USDC, an exchange would need to migrate thousands of trading pairs and attract new liquidity. That is a major hurdle.

Traders benefit from choosing USDT as well. If somebody wants to swap $100 million worth of Bitcoin for USDT, they can typically do so with minimal slippage or price impact. Doing the same with another stablecoin on many exchanges would likely create greater slippage. These are real costs and a strong reason to continue using USDT over a newer competitor.

This creates a feedback loop that is extremely difficult to disrupt. Liquidity attracts market makers and trading pairs, which attract additional users, which in turn attract even more liquidity.

This is why USDC has struggled to materially take market share from Tether within the crypto ecosystem. USDC’s share is increasing, but gradually.

Q4 earnings release; USDC and USDT control 97% of the market.

USDC and USDT dominate 97% of the stablecoin market for a clear reason: money behaves like a network business. The more people use it, the more valuable and attractive it becomes to others.

3. Signs that USDC is decoupling from crypto

USDC’s primary growth driver is the amount of USDC in circulation, also known as circulating supply. As more individuals and institutions use and hold USDC, circulating supply increases.

For Circle Internet Group, the company behind USDC, a larger circulating supply directly increases revenue. Circle invests the reserves backing each USDC token into U.S. Treasuries, so as the market capitalization of USDC rises, earnings rise as well.

Expanding the number of use cases for USDC helps increase circulating supply, which directly benefits Circle’s business model.

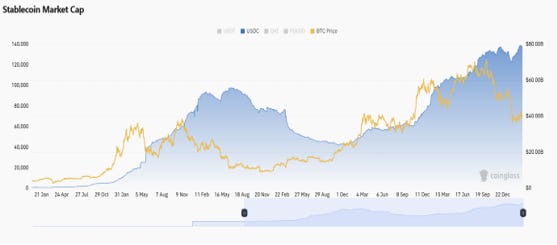

Historically, demand for USDC was closely tied to cryptocurrency trading activity. People frequently used stablecoins to move quickly between crypto assets and dollars. During the 2022 bear market, this relationship became very clear.

Following the collapse of Terra Luna and the failure of FTX, Bitcoin declined sharply, and USDC supply followed. Market capitalization fell from roughly $60 billion to below $20 billion as capital exited crypto and moved back into fiat currencies.

What is different now is the latest drawdown. Despite an approximate 50% decline in Bitcoin since October 6, 2025, USDC’s market capitalization continued rising. This suggests that USDC is increasingly being used for purposes beyond crypto trading alone.

USDC market cap keeps rising during crypto market downturn.

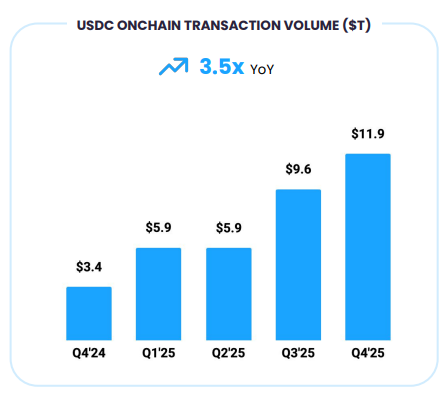

Furthermore, USDC on-chain volume saw sharp sequential increases between Q2 and Q4 of 2025. Q4 marked the beginning of the crypto bear market, yet USDC volume growth continued.

This provides additional evidence that the sources of USDC activity are becoming more diversified beyond crypto.

USDC on-chain volume keeps rising despite crypto bear market in Q4 2025.

In conclusion, USDC increasingly appears to be used for broader financial activity beyond cryptocurrency speculation. As a result, Circle’s revenue may become less dependent on crypto market volatility, potentially making the business more resilient and deserving of a higher valuation multiple.

4. USDC is in an institutional flywheel

The implementation of the GENIUS Act in the U.S. has been an important catalyst for stablecoins. By creating a federal framework for issuers such as Circle, it effectively de-risked USDC for more conservative institutions.

Here are several recent developments involving Circle and institutional adoption:

Deutsche Bank and Standard Chartered are developing infrastructure that facilitates stablecoin-based settlement for cross-border payments. They also serve as custody and on/off-ramping partners for USDC.

In December 2025, Visa adopted USDC for settling payments outside conventional banking hours. According to Visa, growth has been strong, reaching roughly $4.5 billion in annualized volume.

Companies including Cash App, Mastercard, Gusto, and Interactive Brokers have introduced products leveraging USDC.

USDC has become the primary collateral and settlement asset for Polymarket, currently the world’s largest prediction market.

JPMorgan executed an end-to-end transaction involving a $100 million tokenized bond where the proceeds were settled in USDC.

Circle Payments Network, a Visa/Mastercard-like network enabling payments between financial institutions, is scaling rapidly. The network launched in June 2025 and now processes roughly $5.7 billion in annualized volume. Currently, 55 institutions are enrolled, while another 74 are undergoing eligibility review.

As institutional adoption expands, network effects become increasingly important. When one institution adopts USDC, connected counterparties, service providers, and platforms often begin integrating it as well.

This makes adoption easier for future participants and strengthens the ecosystem over time. More integrations lead to greater usage, while greater usage attracts additional integrations.

5. A market built to compound

The global money supply is estimated at roughly $120 trillion, of which around $60 trillion sits in physical cash and demand deposits—essentially payment money and working capital.

The true opportunity is not the entire money supply, but this ~$60 trillion pool. It is capital already designed to move through the global economy, making it the most immediate addressable market for stablecoins like USDC.

Against that backdrop, USDC’s roughly $75 billion market capitalization represents only a tiny drop. Even a relatively small shift in allocation could materially increase circulating supply—and with it, Circle’s revenue.

Growth will likely come from areas where speed, cost, and accessibility matter most, such as international transfers and financial settlement.

AI could also accelerate stablecoin adoption. AI agents are capable of transacting instantly—paying for data, content, or services—and enabling microtransactions that were previously uneconomical due to high fees.

If payments evolve in this direction, stablecoins could capture a larger share of global transactions and, by extension, global payment money. That would create structural demand beyond traditional crypto-related use cases.

Takeaway

The core of the thesis is relatively simple: stablecoins allow money to move across a single, shared system rather than through fragmented banking infrastructure. That can reduce friction, lower settlement costs, and increase transaction speed across payments and financial markets.

This is why institutions are increasingly adopting stablecoins and integrating them into their systems. USDC appears particularly well positioned because of its regulatory framework and growing institutional adoption.

What makes the opportunity interesting from an investment perspective is the size of the market. Stablecoins are targeting a global pool of roughly $60 trillion in payment money and working capital. Even small shifts in adoption could materially expand USDC’s circulating supply and, by extension, Circle’s earnings power.

For that reason alone, I believe this is a space worth watching closely.

Disclaimer

This article reflects my personal views and is for informational purposes only. It is not financial advice, and nothing here should be considered a recommendation to buy or sell any securities. Please conduct your own research and consider your own financial situation before making any investment decisions.